The First Tier Tribunal Tax Chamber (FTT) have held that a dilapidated bungalow is not a single dwelling for SDLT purposes. Judge Richard Thomas William Haarer concluded that the test for “used or suitable for use as a single dwelling” (wording contained in paragraph 18(1) Schedule 4ZA of the Finance Act 2003), was, whether as at the date of completion of the purchase, the building in question was suitable to be used as a dwelling not whether the building is capable of being a dwelling.

The Claimant’s purchased the building in question for redevelopment. The consideration for the building was £200,000. On completion, the Claimant’s solicitors filed an SDLT return for £1,500.00, HMRC claimed that the SDLT payable should have been £7,500.00 (being the higher rate payable for additional residential property).

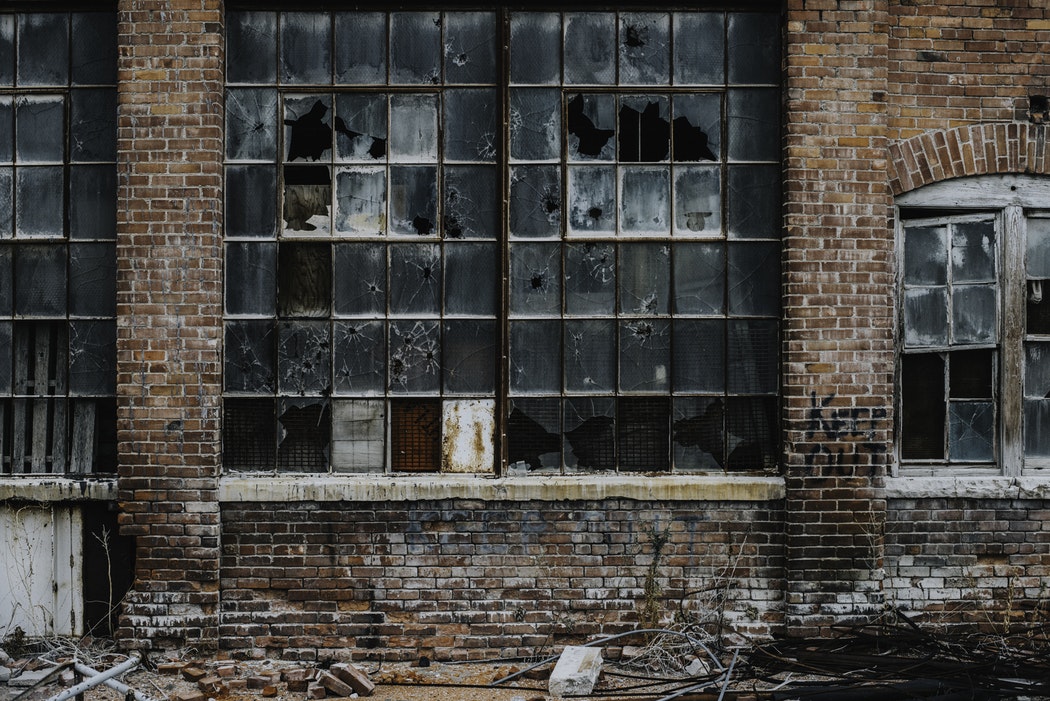

The Claimant showed the FTT evidence of radiators and pipework removed and given that asbestos was present preventing repairs or alterations the FTT held the bungalow, as at completion was not suitable for use as a dwelling.

The Claimant’s solicitors used the rubric code 01 (Residential) as to the use of the property on the SDLT return, the FTT stated that the correct rubric code was 03 (Non-residential).

The FTT held the correct amount of SDLT payable was £1,000.00.

The case highlights the need for clear and concise SDLT advice in relation to any transaction, if you are a developer requiring assistance throughout the redevelopment/construction process, please contact Simon Walker at Talbot Walker LLP.

For the full judgment: http://financeandtax.decisions.tribunals.gov.uk/judgmentfiles/j10915/TC06951.pdf